The New York Times is wrong, inflation won’t save you money on your taxes

According to the New York Times, there is one silver lining to inflation; it will save you money on your taxes next year.

Why is that the case?

That’s because the federal government annually adjusts many elements of its complex tax code, including the standard deduction and tax brackets, to reflect inflation and avoid so-called stealth tax increases.

The NYT uses this example to illustrate this point.

This year, the middle federal tax rate of 24 percent applied to ordinary income over $89,075 for a single filer and over $178,150 for a couple filing jointly. Next year, the income thresholds for that bracket are projected to increase to about $95,375 for single taxpayers and $190,750 for couples. (The Internal Revenue Service usually announces official numbers in late fall.)

But is it true that inflation saves you money on taxes? Not exactly, and here is why.

Why tax brackets are adjusted for inflation

According to the Bureau of Labor Statistics (BLS), in August prices were up 8.3 percent compared to last year during the same time. So, using that rate of inflation, $95,375 this year is worth approximately only $88,065 at the same time last year.

So, if you made $88,000 last year, and you make $95,000 this year, it might appear that your income has gone up. However, in real terms, the value of your money has gone down quite considerably.

And if the Federal government did not index the tax brackets to inflation, you would move into a higher income tax bracket, and thereby pay more taxes as your nominal income grows, even if the real value of your income — or your ability to pay — was going down.

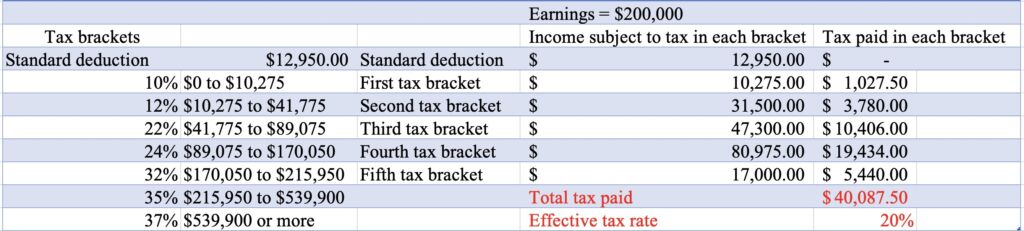

Consider a taxpayer who makes $200,000 before inflation. Using current tax brackets, a single tax filer making $200,000 would pay 20 percent of his income in taxes.

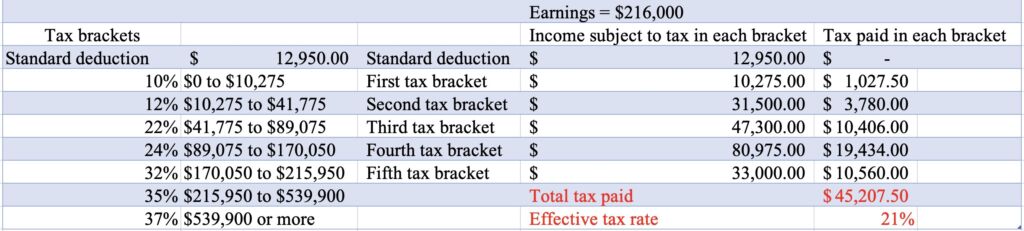

But if this person’s income went up to $216,000 — due to 8.3 percent inflation —, under the same tax brackets, he would pay 21 percent of his income in taxes. That is, even though in real terms his income hasn’t gone, his effective tax rate has gone up.

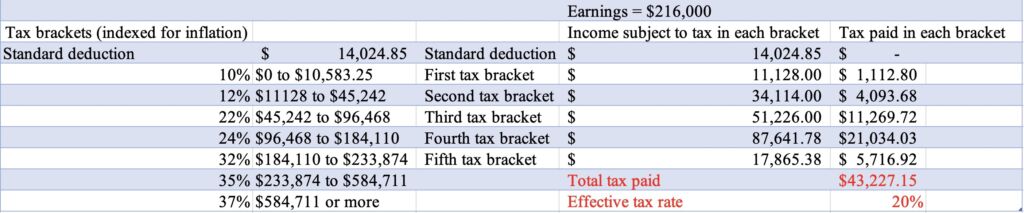

That is why the government indexes the tax brackets to inflation in order to remedy this bracket creep, as it is known. In fact, when we index the tax brackets to reflect the 8.3 percent inflation, the taxpayer remains at his original effective tax rate of 20 percent.

Inflation won’t save you money on your taxes

The United States has a progressive tax system. That is, as your income — or ability to pay grows — the effective tax rate that you pay also grows. But if your income is rising due to rising prices, it does not mean that you are richer. In fact, if your income grows at a lower rate than the rate of inflation, you become poorer — that is your ability to pay diminishes.

With rising prices, your money is worth significantly less than it was a year ago. Adjusting the tax brackets for inflation only reflects that reality, and ensures that you do not get pushed into an upper tax bracket — and pay more taxes — as your nominal income grows

The New York Times is wrong; adjusting for inflation is not going to save you money on your taxes. At best, you will pay the same effective income tax rate as before — that is also only if we assume that the IRS will adjust for the true rate of inflation. Otherwise, if the IRS adjusts tax income brackets by 7 percent while inflation has gone up by 8.3 percent, you will still wind up paying more in taxes than the previous year.