Inflation: What did cause it?

Yesterday I looked at popular explanations for America’s current inflationary woes and explained why they weren’t, in fact, its causes. So what did cause it?

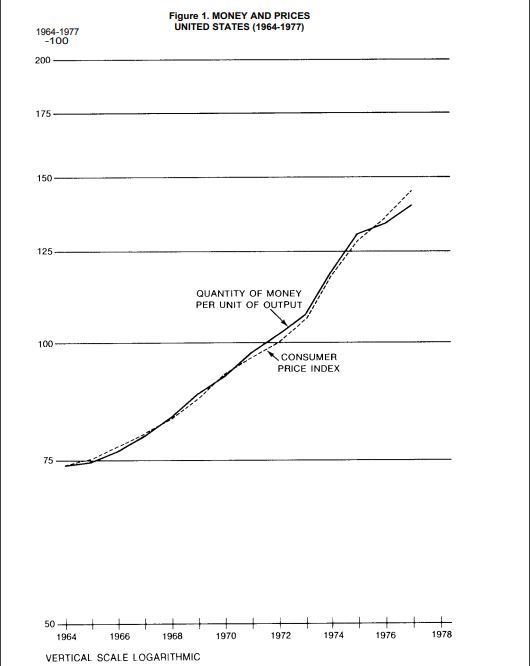

As I wrote last October, the economist Milton Friedman observed a close relationship in the historical data between the growth rate of the money supply and the rate of inflation. Figure 1 comes from his book Free to Choose:

Figure 1

From this relationship, Friedman argued that:

Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.

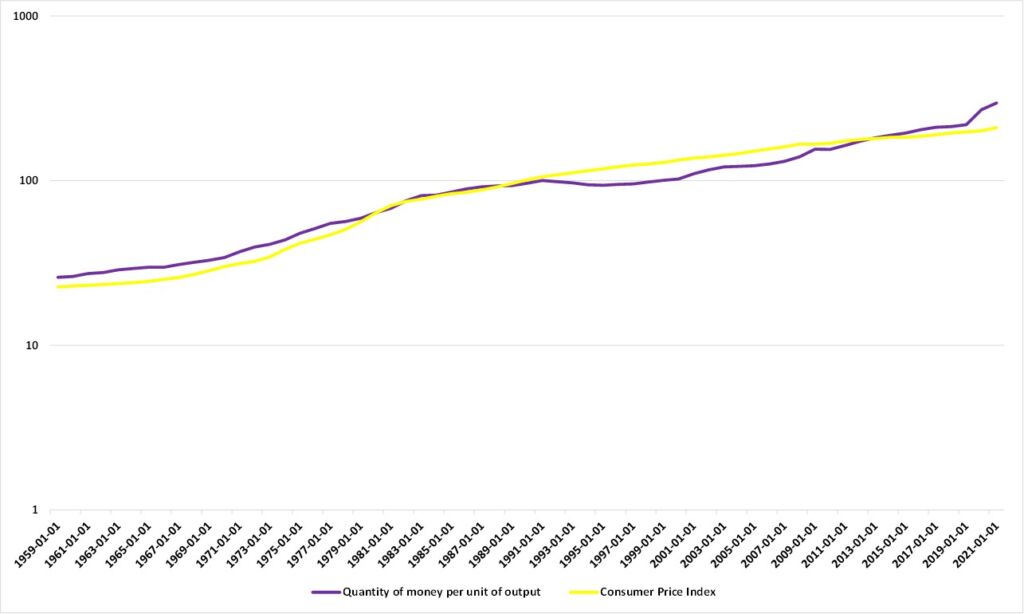

This goes far towards explaining our current inflationary problems.

Figure 2 recreates Figure 1 and extends it. We see a fairly close relationship between the two series over an extended period of time, with a stark divergence in the last 18 months.

Figure 2: Money and prices in the United States (1960-2021) 1960-2021=100

What has driven that divergence? Remember that Quantity of money per unit of output is derived by dividing the M2 money supply by Real GDP. As I wrote in March, “Changes in the ratio of M2 to real GDP can be driven by changes in either — or both — of M2 or real GDP.”

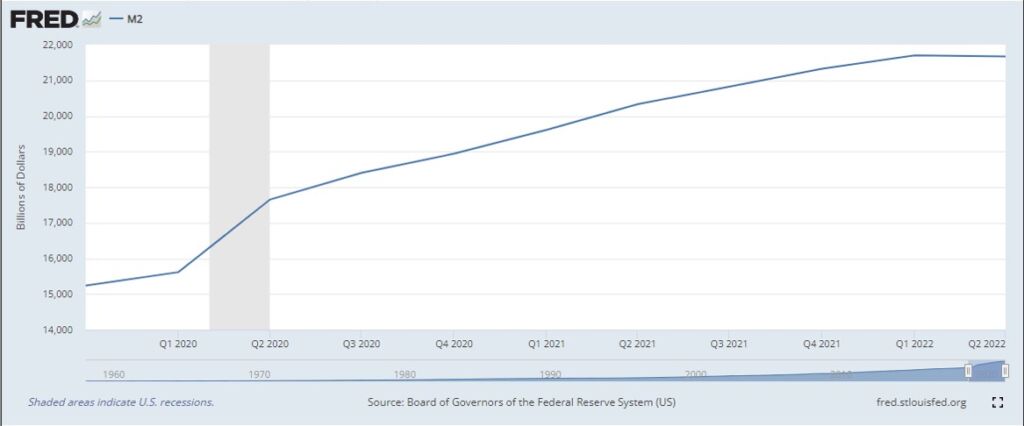

Yesterday we saw that Real GDP rose by 2.7% from the fourth quarter of 2019 to the first quarter of 2022. As Figure 3 shows, however, M2 increased by 42% over the same period.

Figure 3

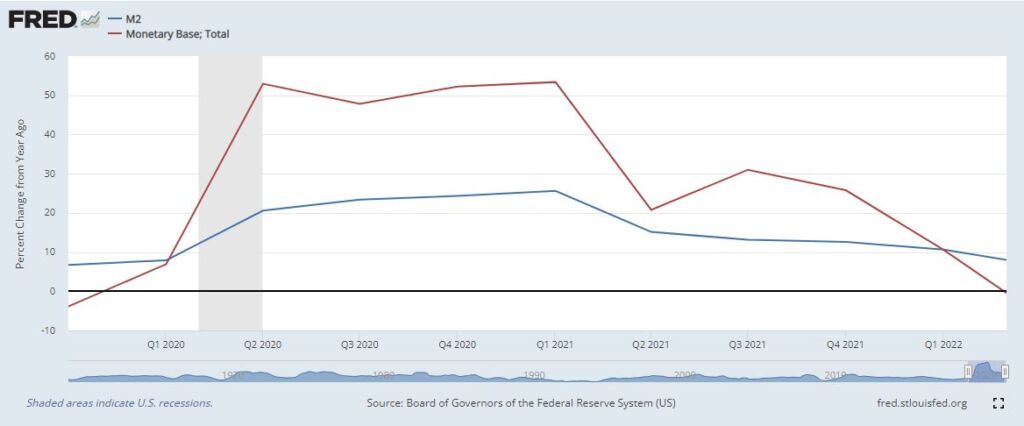

This, in turn, was driven by an increase in the Monetary Base of 82.9%, as Figure 4 shows.

Figure 4

In short, in early 2020, as COVID-19 hit, the Federal Reserve began printing up money, expanding the Monetary Base, and using it to buy assets. This fueled growth in the broader monetary aggregate M2, faster than the growth of the quantity of goods and services there were available to spend it on — Real GDP. That is the cause of out current inflation.

This framework gives us a way to think about what might happen next. I’ll discuss that tomorrow.