Corporate and sales tax reforms can boost North Dakota’s economy

Yesterday, I wrote about how North Dakota’s policymakers should look to the tools they have — notably control over state taxes — to boost economic growth in the face of the Biden administration’s war on American energy production, which is hitting the state’s economy particularly hard.

What fiscal policy scope do the state’s policymakers have?

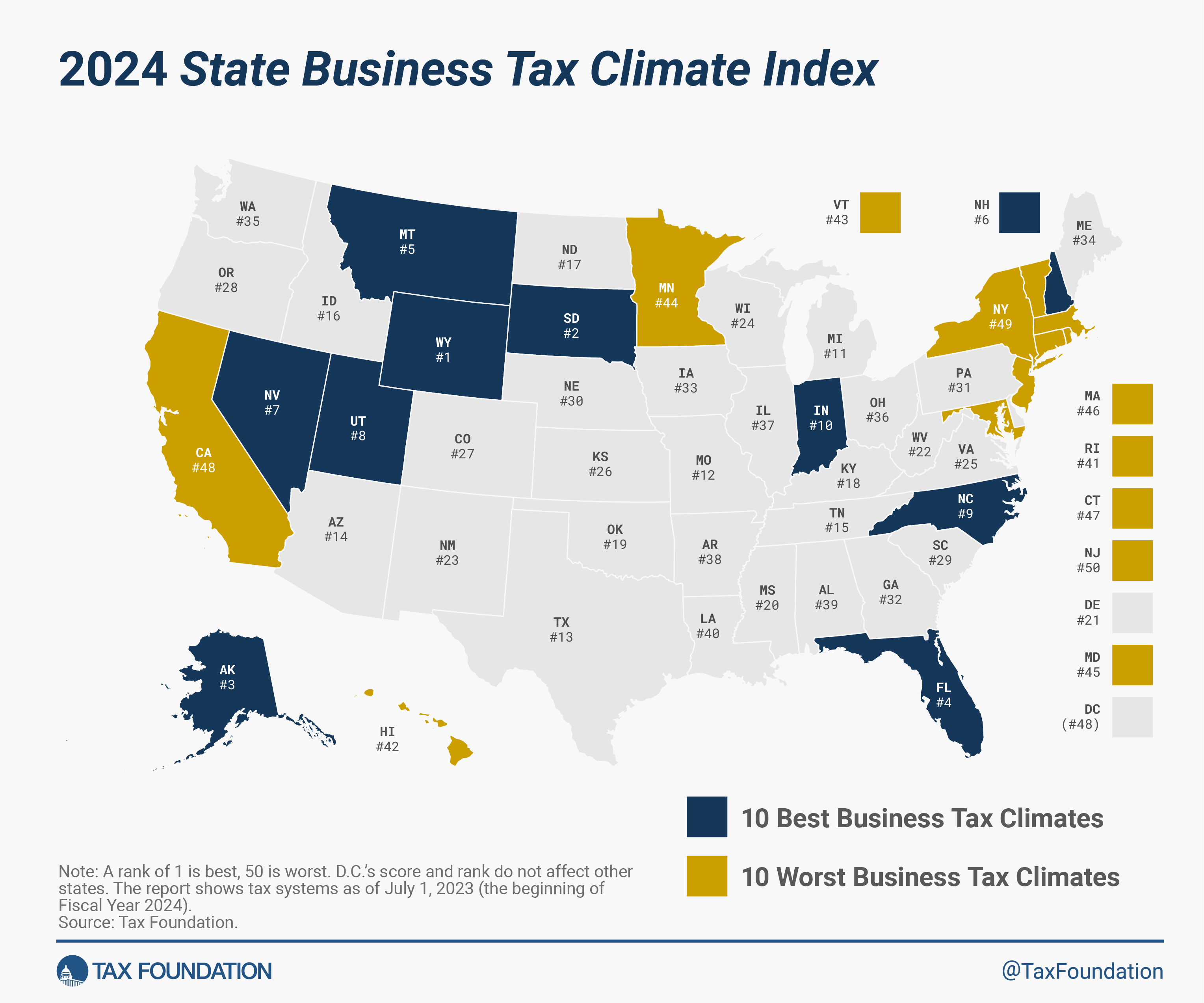

The Tax Foundation’s 2024 State Business Tax Climate Index ranks North Dakota 17th. That isn’t bad, its certainly better than Minnesota, but there is room for improvement.

Sales tax

North Dakota scores its lowest ranking on the sales tax — 32nd. As I wrote in “A Plan for Corporate Tax Reform in North Dakota” in November 2022:

…the burden of a state’s sales tax isn’t just a function of the rate but of the base. States which exempt many goods and services from the sales tax are said to have a “narrow” base and those which do not offer many such exemptions are said to have a “broad” base. North Dakota’s sales tax has a base so broad that it includes many business-to-business transactions.

This isn’t good:

Sales taxes are generally favored by economists because, as they are levied at the point of sale, they are less likely to cause economic distortions than taxes levied at some intermediate stage of production. This is not the case if the sales tax is imposed on business-to-business transactions, or business inputs. Research has found that sales taxes levied on equipment have a negative effect on small business startups and have incentivized companies to avoid locating factories or facilities in certain states because the factory’s machinery would be subject to the state’s sales tax.

Out of the 50 states and the District of Columbia, 36 of these 51 jurisdictions impose a sales tax. North Dakota is one of only ten not to fully exempt farm equipment; it is one of only nine not to exempt manufacturing machinery; it is one of only twelve not to exempt business fuel and utilities.

“The ideal base for sales taxation is all goods and services at the point of sale to the end-user,” I concluded, so “North Dakota should exempt business inputs from its sales tax.”

Corporate tax

North Dakota scores better for its corporate taxes – 10th. But here, too, there are basic things which can be done to improve this ranking.

As I wrote in 2022:

Thirty out of the 45 jurisdictions in the United States that levy a corporate income tax impose a flat rate. Fifteen states, however, have multiple-bracket corporate income taxes, and North Dakota is one of these.

Where a jurisdiction does impose a corporate income tax with multiple-brackets, it is important to index the brackets for inflation. Without this, a nominal increase in corporate income can impose a real increase in the corporate tax burden: what is known as “bracket creep.” This “inflation tax” is levied without anyone’s consent.

This problem is especially acute when, as now, inflation is running at elevated levels. To fix this, I concluded, “North Dakota should index its corporate income tax for inflation, as is done annually with the state’s individual income tax brackets.” Beyond that, it should move to a flat rate of corporate income tax.

A further problem with North Dakota’s corporate taxes is that it is one of 20 states and the District of Columbia that have a so-called “throwback rule.” In a deeply integrated economy like that of the United States, the question of where to tax corporate incomes is a difficult one. The Tax Foundation explains:

States can only tax corporations that have economic nexus with the state, which means that the corporation must have sufficient connection to the state to justify taxation. However, federal law constrains states in defining economic nexus. More specifically, Public Law 86-272 prohibits states from taxing income that arises from the sale of tangible property into the state by a company that has no other activity in that state other than soliciting sales.

When companies sell into a state where they do not have nexus, that destination state lacks jurisdiction to tax the company’s income. This results in what is known as “nowhere income”—income that cannot legally be taxed by the state where the income-producing sale occurs.

Under throwback rules, sales of tangible property which are not taxable in the destination state are “thrown back” into the state where the sale originated, even though that’s not where the income was earned. This means that if a company located in State A sells into State B, where the company lacks economic nexus, State A can require the company to “throw back” this income into its sales factor.

Since two or more states can theoretically lay claim to nowhere income, however, complicated rules have to be created and enforced to decide who gets to tax it. Because of this, throwback rules add yet another layer of tax complexity. The Tax Foundation explains that throwback rules:

…have a notable impact on business location and investment decisions and reduce economic efficiency for the states which impose such rules. Over the long run, these rules reduce competitiveness while yielding very little—or no—increase in state collections.

To resolve this, I concluded in November 2022, “North Dakota should repeal its throwback rule.”

None of these measures is, perhaps, all that eye catching. But they would boost North Dakota’s scores on these measures significantly and that is something businesses would notice.